September 2017

Several legislators are proposing approaches known as Medicare or Medicaid buy-ins that would incrementally expand access to those public programs and, in theory, make insurance more affordable. According to a Kaiser Family Foundation poll in September 2017, these incremental affordability ideas may be more popular than single-payer approaches. In this post, I explore the pros and cons of each and who would be best helped under each program.

The biggest problems with expanding access to Medicare or Medicaid is to whom we are expanding access and the expenses they bring with them. These costs can either be absorbed by the individual, the government, or some combination. The individual market is expensive for a number of reasons — in part because utilization and risk are high — and adding these individuals to public programs requires the public to bear at least some of those costs.

The same goal — absorbing a costly, riskier population into a larger group — could be done by creating collaborations with the Department of Defense, the Office of Personnel Management (the federal government’s Human Resources Department), or any state employee offering. It doesn’t need to be Medicare or Medicaid — it needs to be a large purchaser that can absorb the administration.

To be clear, the Medicaid and Medicare buy-in efforts largely do not compete with one another. They are both incremental and address different needs for different populations. These approaches are also fairly different from Senator Sanders’ Medicare for All approach, which is more of a take-down of the current system. The following two approaches could each play an important role in offering high-value, affordable healthcare to all.

Medicare buy-in

These offerings usually involve expanding access to Medicare by allowing people under 65 (the current eligibility threshold) to start eligibility early, possibly by paying extra premium contributions to offset the early entry. Usually the recommended range is 55–65 years old.

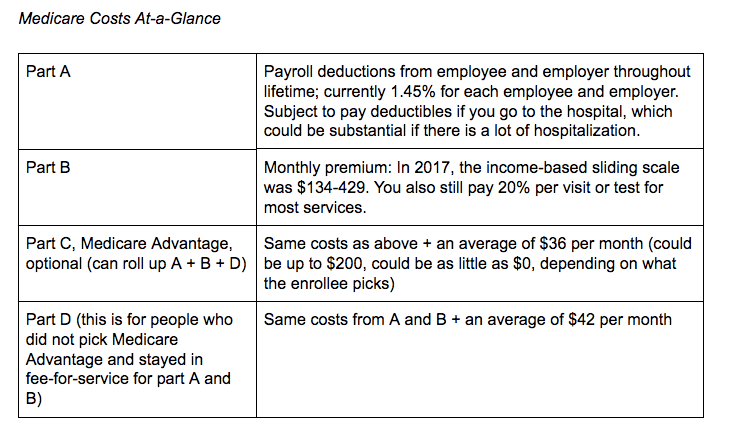

Right now, the way Medicare generally works for most people is that you (or your spouse) work for 10 years (40 quarters) and then you and your employer have paid enough Medicare payroll taxes for you to get Part A coverage, which means you can go to the hospital, but you’ll pay a deductible when you do. Optionally, you can buy Part B coverage for doctor’s office, therapy, imaging, lab tests, etc. You can pay a monthly premium, calculated on an income-based sliding scale, that is currently between $134-$429 per month. You must also pay 20% cost-sharing for most of these covered services. (Note: There are so many exceptions to all of this, but I’m trying to keep it high level and relative to this discussion.)

Prescription drug coverage is through Part D, which is a managed care plan. The average cost of these plans in 2017 is another $42/month. You can also get all of this rolled up into a Medicare Advantage plan, which is a managed care plan, and pay anything from nothing more to a lot more, depending on whether you choose a narrow network HMO type plan or a lot of flexibility with a PPO. In any case, these plans usually help limit the cost sharing, but there are trade-offs in terms of network flexibility.

Medicare benefits are oriented towards the populations they serve: seniors, people with disabilities, and with end-stage kidney disease. Medicare does not cover long term nursing home care, dental care, or eyeglasses. Everything about Medicare — the provider network, quality measures, data systems, payment models, demonstration models, licensing and certifications, and reimbursement — is based on the benefits for this population. Adding new populations with additional needs for benefits may bring serious considerations for the administration of these changes. This is typically why 55-years-old might be the youngest this policy solution could go without substantial program changes.

Buying into Medicare connotes an individual (or their spouse) would have their 10 years of work credits, then would pay their Part B premium. While this is a for-cost expenditure for the Medicare program — these individuals are less likely to be contributing Medicare payroll taxes, more likely to be retired, and they are more likely to utilize benefits — this group has a harder time obtaining affordable insurance and raises costs on the general risk pool in the individual market. However, this lever could only be used at the federal level (no option for states to pursue) and would require statutory changes and appropriations. Notwithstanding, making options like Medicare buy-in available for seniors may make insurance cheaper on the individual market and this is an option we should continue to explore.

Medicaid buy-in

Most states let people with disabilities buy into Medicaid in some way. To be sure, these programs for people with disabilities are not the full-fledged, comprehensive, open-ended buy-in that would be offered to anyone who lacks insurance. Nevada and Minnesota have seriously discussed allowing for these more comprehensive Medicaid buy-ins, but have not yet passed laws.

People who work in Medicaid like to say, “You’ve seen one Medicaid and you’ve seen one Medicaid program.” It’s a cheeky way to say that the program is a federated model where 56 states, the District of Columbia, and five U.S. territories all run different programs, and under that, different programs for different populations. There are different rules for eligibility for different people, different benefit sets and providers, a multitude of grants, and different delivery systems: sometimes managed care plans, sometimes fee-for-service, and sometimes hybrid models. In other words it’s not easy to explain what one would be buying into because it would no doubt vary state-to-state. However, my best guess is that most states would make available what they are required to offer the Medicaid expansion populations — that is, the Essential Health Benefits. This would allow premiums to be as cheap as possible, while still giving an individual the most needed benefits.

Most of the programs states run for the Medicaid expansion populations are through managed health plans. The majority of the Medicaid program is delivered this way. The premium is not going to be as affordable as most people might want — it’s still probably going to be several hundred dollars per person, depending how you segment age bands and any other risk — but people would avoid the utilization-prohibitive deductibles and cost-sharing that they are encountering in the individual exchange market. Medicaid programs, by law, have no serious deductibles or cost-sharing and the program is quite easy to access and understand. Satisfaction rates are high with Medicaid enrollees.

Interestingly, we have a good idea of what this might look like and for the right set of benefits tailored to the Essential Health Benefits because several states put their expansion populations on the federal Obamacare ACA exchange. Medicaid buy-in would be sending many similar people back the other direction from the exchange to the state. So conceivably we could have Medicaid enrollees on the exchanges in some states and and Exchange-eligible individuals buying into Medicaid in other states.

There are two ways Medicaid buy-ins can happen: A state can pass legislation or the federal government can pass legislation. As discussed above, states like Minnesota and Nevada have recently made an effort. We expect there to be a bill introduced soon in the U.S. House of Representatives as well. The vehicles to implement programs like this already exist — section 1332 and 1115 waivers are very flexible. The problem is the willingness in the states and in HHS to authorize and implement these programs.

Nonetheless, what would this look like? This could be a reasonable insurance program for most people in states where the Medicaid program is well-run and providers are fairly compensated. At least initially, individuals would probably pay the full premium (no state responsibility), but — in theory — their utilization, risk, and administrative costs get absorbed by the larger population. As previously mentioned, this method leaves the state subject to a substantial movement of risk and utilization onto the state enrollment. This means that all premiums would increase — possibly only on the margins — depending who and how many people chose to take up Medicaid as an insurance option. A second option would be to segment the risk and utilization, making this population rated separately, and only absorbing the administration (which is not insignificant). Premiums would probably continue to remain high for awhile.

This policy approach leaves room to start getting people coverage, then subsidize for affordability. The Medicaid market is going to exist whether or not extraneous people purchase coverage, so the stability of this market is a strength.

*******

Overall, both the Medicare and Medicaid buy-in options are two strong levers for incremental delivery system reform goals at the national or state level. Both levers would supplement the goals of the ACA and could continue to strengthen the individual market. Here are some additional links on ongoing efforts:

Medicare buy-in efforts

- “Medicare at 55 Act”: Introduced by Sen. Debbie Stabenow (D-MI) in August 2017

Medicaid buy-in efforts

- Nevada’s “Sprinkle Care”: Vetoed by Governor Sandoval in June 2017

- Rep. Brian Schatz (D-HI): Upcoming legislation

- Minnesota: MinnesotaCare buy-in