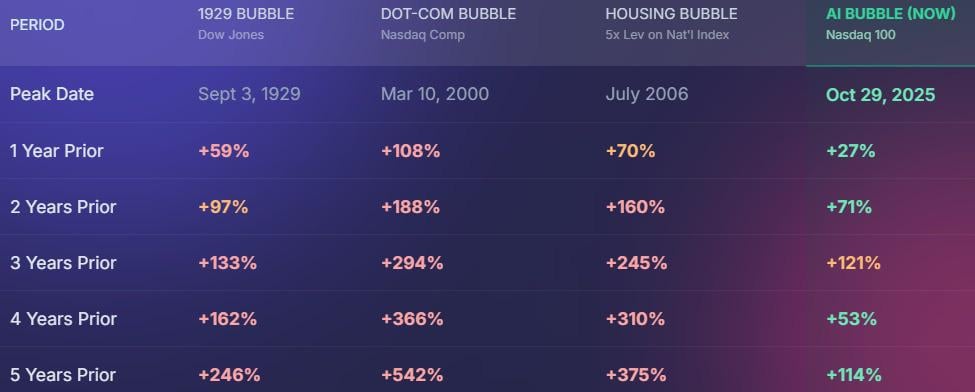

Bulls keep winning and bears keep getting wrecked for one simple reason: most bears are fighting the last war. They’re staring at 1999-style trailing P/E charts or pre-1990s valuation norms and declaring “this time is different” as if that’s automatically a bad thing. In reality, this time really is different – and the data backs it up.

Look at the Magnificent 7 specifically:

• Forward P/E ratios are surprisingly moderate given the growth rates we’re seeing

• PEG ratios (P/E divided by expected growth) are actually lower than they’ve been at many points in the past decade and significantly lower than the rest of the S&P 493

We’re not paying 1999 multiples for 1999 growth – we’re paying reasonable (or even cheap) multiples for a completely different quality of business.

The core reason we’ll never return to pre-1990s valuation levels: the economy has shifted from tangible to intangible assets. Intellectual property, network effects, proprietary datasets, and software moats compound in ways steel mills and railroads never could. These assets get better and cheaper to scale every year instead of depreciating.

On AI specifically – the bear case that “AI won’t monetize” misses the bigger picture. Direct AI revenue might concentrate in a handful of players (Nvidia, the cloud hyperscalers, etc.), but the second-order effect is massive OPEX compression across every industry. Translation: companies will need far fewer employees to generate the same (or more) revenue.

You might lose your job… but the companies you own will be dramatically more profitable because of it. “You’ll own nothing, be replaced by a model, and be happy.”

Bears who keep waiting for a return to 15× earnings are going to be waiting a very long time. The game changed permanently sometime around the mid-90s and the laggards still haven’t adjusted their mental models.

Look at the Magnificent 7 specifically:

• Forward P/E ratios are surprisingly moderate given the growth rates we’re seeing

• PEG ratios (P/E divided by expected growth) are actually lower than they’ve been at many points in the past decade and significantly lower than the rest of the S&P 493

We’re not paying 1999 multiples for 1999 growth – we’re paying reasonable (or even cheap) multiples for a completely different quality of business.

The core reason we’ll never return to pre-1990s valuation levels: the economy has shifted from tangible to intangible assets. Intellectual property, network effects, proprietary datasets, and software moats compound in ways steel mills and railroads never could. These assets get better and cheaper to scale every year instead of depreciating.

On AI specifically – the bear case that “AI won’t monetize” misses the bigger picture. Direct AI revenue might concentrate in a handful of players (Nvidia, the cloud hyperscalers, etc.), but the second-order effect is massive OPEX compression across every industry. Translation: companies will need far fewer employees to generate the same (or more) revenue.

You might lose your job… but the companies you own will be dramatically more profitable because of it. “You’ll own nothing, be replaced by a model, and be happy.”

Bears who keep waiting for a return to 15× earnings are going to be waiting a very long time. The game changed permanently sometime around the mid-90s and the laggards still haven’t adjusted their mental models.