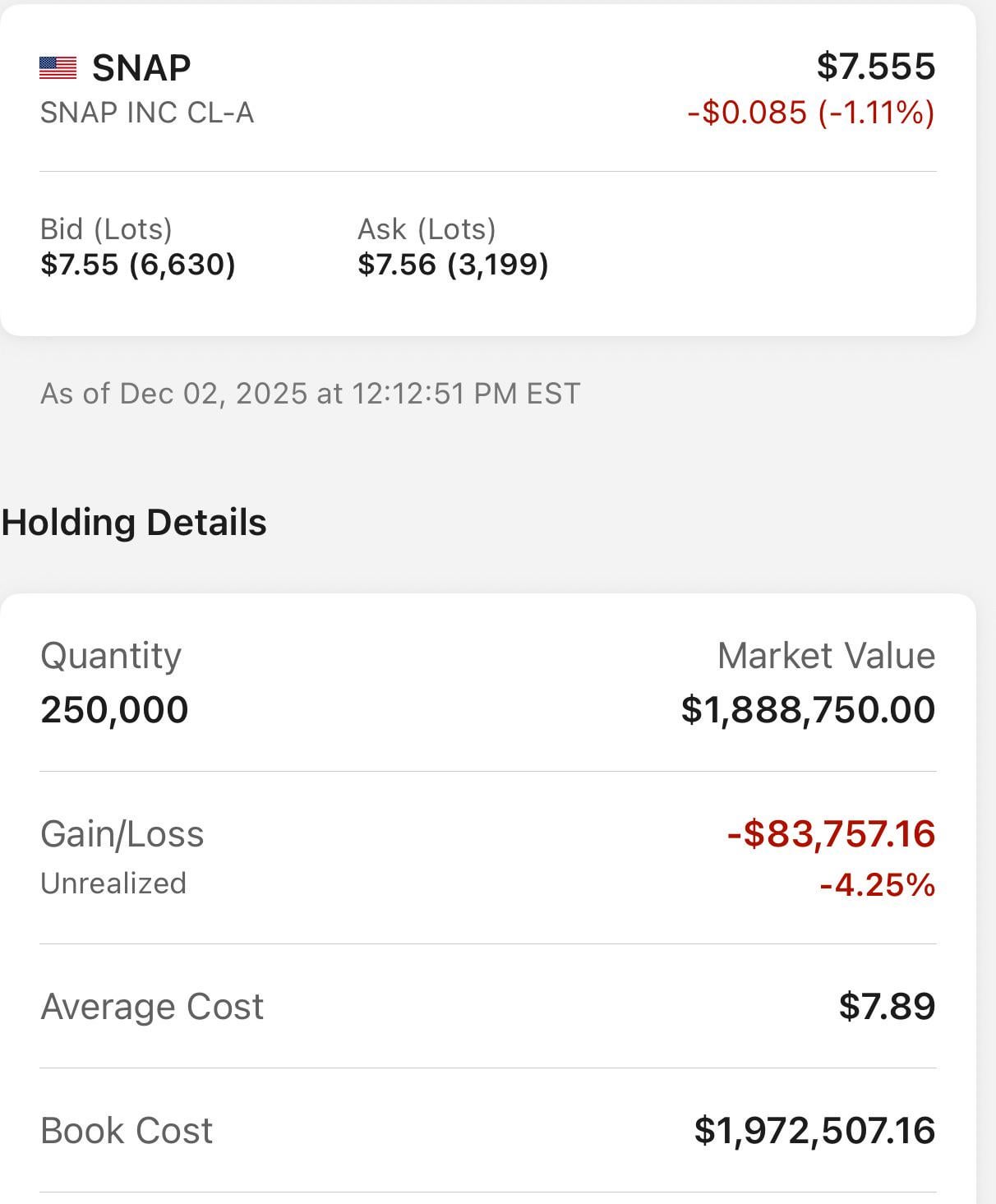

I invested in SNAP earlier this year more as a trade and sold after the spike post-Q3 earnings, making about $200k. However, I now look at SNAP as more of a longer-term investment, and my thesis follows:

Since inception, SNAP has been an awful investment mainly because they can’t make money, which is somewhat important for a business to be able to do. It faces the following issues:

-Founders control the voting rights and haven’t been the best capital allocators.

-Egregious stock-based comp has diluted shareholders.

-Best features (like Stories) copied by META and monetized much better.

-Ad stack worst-in-class.

-Very high operating costs, mainly due to infrastructure.

-Young users, hard to monetize due to lack of purchasing power.

-Growing fast mainly in low-income countries like Indian and Pakistan, yet flat to slight decline in North America and Europe.

SNAP, as Spiegel mentioned recently, is at a crossroads. It can die a slow, unprofitable death, or it can innovate and start to make money for once. It seems that the company actually gives a damn about monetization now, and I will mention why below:

-Started offering various subscriptions, including Snapchat+, Memories Storage, Lens+, and Platinum. Subscription revenue is currently annualized at $750 million / year for now and is growing double digits, which is unique among its peers. I particularly like the Memories Storage Plan, as it takes a cost center and turns it into a profit center, such as Icloud storage, Google, etc…Many users may now want to lose the invaluable pictures and videos they have stored there. The download and import process isn’t that easy, and there will be friction. A certain number of users will say “screw it, I’ll just pay a couple bucks a month for it”. Meanwhile, the users that do not pay for it will be limited in storage, thus SNAP will limit their data storage expense.

-Spiegel recently mentioned that they would put profits slightly above user growth and engagement. After all, what use is having hordes of users if you cannot make money off of them? Sometimes, you indeed have to “fire” your customers.

-They have increased space for ad inventory recently with their Spotlight feature, as well as Sponsored Snaps, with the latter improving margins as well even though there was surely some resistance internally over sticking ads in the messages. The fact that Sponsored Snaps won out and was not vetoed shows the seriousness of management in using all available levers to increase revenue.

-They recently reorganized into small, nimble teams in order to innovate and ship faster and bypass bureaucracy. The Snapchat+ success was created by a small team, for example, so they decided to scale this operationally company-wide.

SNAP has invested billions in its AR tech, and while the jury is out on whether AR will ever become a “thing”, I think we can safely say that SNAP is at the forefront of the technology. They have the most used AR products in the world, and they are marrying their software to hardware with the release of their Specs next year. Rumor is that they are looking for a partner as it will require a lot more capital to become a consumer product sitting on shelves, which is also a positive as I don’t want them touching those billions sitting in their bank account. Personally, I do not feel that the AR glasses will be a commercial success, mainly because SNAP has no record of being successful in hardware. I look at the Specs as a free call option in case they actually end up doing well. If they bomb, then perhaps SNAP will stop committing so much capital to them going forward, which would also be a positive.

What investors need to think about is this: How difficult is it to create a product that has over 400 million DAU and almost 1 billion MAU? SNAP has that, yet only has a $13 billion market cap. Ideally, the company would be absorbed by a larger player as an acquisition would be immediately accretive to their financials. Opex would plummet since a MS or META or GOOG would have much lower hosting costs, a better ads platform, and employee headcount would also shrink dramatically. However, I’m not playing this story that way since Evan and Bobby have supervoting shares, and a takeover won’t happen unless they want it to happen. More likely would be if they teamed up with some GCC capital and did a management buyout.

Regarding stock-based comp, dilution as a percentage of revenue has dropped, and while it is still relatively high, management is very sensitive about it and I think it has peaked. They recently announced a $500 million buyback, and I think we will see more to come.

As for the recent $400 million Perplexity deal, I see it as a one-off and don’t ascribe much value to it, for now, especially since Evan said they won’t sell advertising against the chatbot results.

In conclusion, I think the monetization efforts are heating up and 2026 could be a real turnaround year. I don’t have a target price on the stock per se, but it could become a $100 billion company if they can continue to boost margin and topline as they should.