It’s already October, and this is the tenth month that I’ve been writing company analysis on Seeking Alpha. The fiscal year in the US ended at the end of September, and I decided to take this opportunity to report on my work. I decided to give you a report on my recommendations made in the past fiscal year. After all, it is important not only to give recommendations, but also to look back and evaluate previous analyses.

Recommendation — Buy

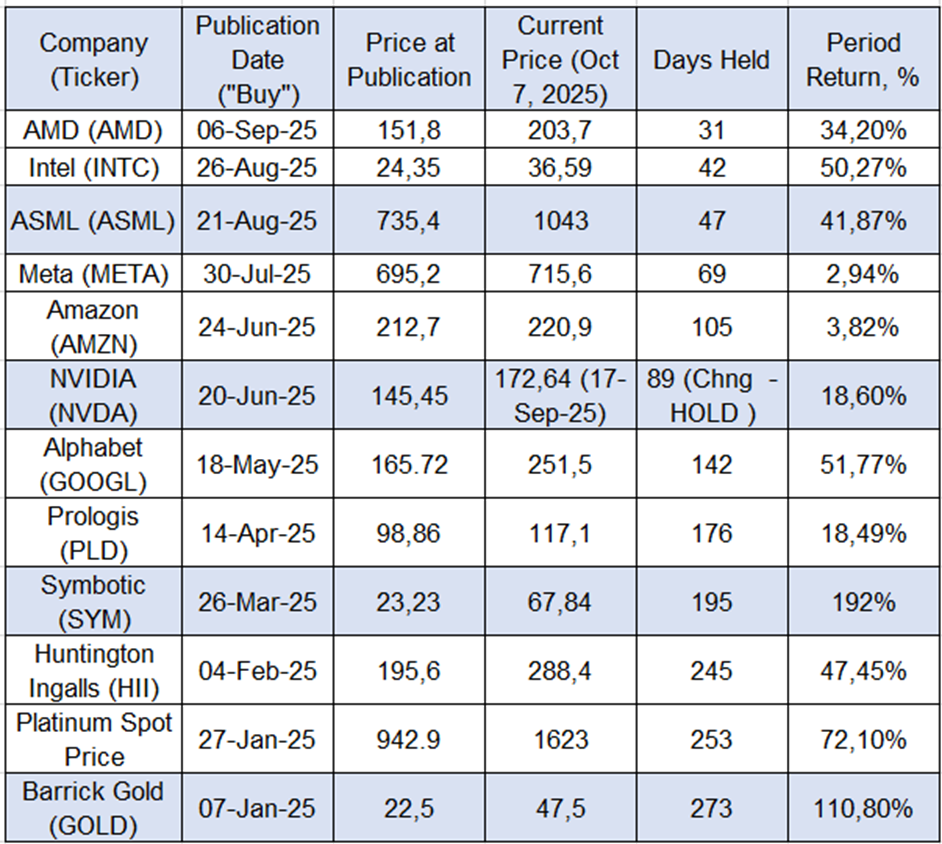

Below you can see a table showing how the prices of stocks for which I gave Buy and Strong Buy recommendations for individual companies have changed. This selection does not include articles on macroeconomics and general market trends.

Performance Review Table

(Closing price for NVIDIA is as of September 17, 2025, the publication date of the article changing the recommendation to “Hold”.)

Overall, I am satisfied with the result. The average return on 12 positions was +53.6%, based on a simple arithmetic percentage. If we convert these figures to annual returns, taking into account the holding period, the average value will be even higher.

Next, I would like to briefly go over my recommendations, describing the essence of the analysis:

AMD (+34.20%) — The idea behind the purchase is that technology giants will buy AMD chips to maintain competition in this market. Secondly, the first significant results after the chip’s announcement may only appear in early 2026, due to the time lost in customer decision-making, testing, and production queues.

As for Intel (+50.27%), I believe that the Taiwanese government’s policy of creating a silicon shield limits TSMC’s ability to compete in the US market. This gives Intel a chance to successfully implement its strategy of building new factories in the US. The company will be able to fill them with orders in the future.

As for ASML (+41.87%), the idea here is simple. The whole world depends on this company. It is a critical bottleneck for the entire technology industry. But at the same time, it was unfairly traded at European P/E multiples rather than American ones. But I think the US will protect this company more than most of its American companies. This means that the risk factor for this company is closer to America than to Europe.

I believe that Meta (+2.94%) has the most futuristic and creative strategy for AI development. But it is lagging behind in implementing this strategy. And I think that when the company manages to fully launch its AI, it can quickly take a strong position by leveraging its huge customer base.

In my opinion, Amazon (+3.82%) has the most pragmatic approach to AI development. They are focused on AWS and B2B customers. This is the easiest and fastest way to get results.

Initially, like many in the market, I viewed NVIDIA (+18.60% in 89 days) as an indispensable bottleneck for the industry for many years to come. This would imply rapid profit growth going forward. But later, I saw a threat from custom chips. Their development could shake the company’s position. Therefore, I changed my recommendation to Hold.

Alphabet (+51.77%) is probably my favorite in the AI race. Until now, the market feared that the company could lose part of its search market share due to the Microsoft/Open AI and Apple partnership. I saw that Gemini had caught up with ChatGPT in terms of quality, which, in my opinion, is a key factor in protecting its markets and actively expanding, taking advantage of its enormous size and market position.

Prologis (+18.49%): I viewed this warehouse real estate giant as a direct beneficiary of trade wars and the reshoring trend. My logic was that the complication of supply chains would lead to increased demand for modern warehouses in the US.

As for Symbotic (+192.00%), I think I was spot on. In my analysis, I wrote that this company is a leader in the implementation of AI in warehouse logistics. But its main problem is that it has only one major customer, Walmart. If the company finds new customers, it will see strong growth. And after my article was published in March, the company found a new customer. In addition to Walmart, C&S Wholesale Grocers became their second largest customer. This was the basis for the explosive growth of the company’s shares.

Last winter, I suggested buying Huntington Ingalls (+47.45%). I assumed that political tensions and the new president, Trump, would lead to increased spending on the construction of warships. And this company builds aircraft carriers. And my prediction came true! Congress allocated money for ships, and thanks to this, Huntington Ingalls’ order portfolio grew.

A year ago, there was already a shortage of platinum (+72.10%) on the market, and this was bound to affect the price, which is exactly what happened.

Problems in Africa dragged down Barrick Gold (+110.80%). But I argued that the rising price of gold would offset these problems. That’s what happened in the end.

Change in recommendations

Using this article, and so as not to write separate articles on changing my recommendations. Here I will withdraw some of my recommendations so that everything is clearly laid out in my feed.

I am changing my recommendation on Amazon to Hold. The reason is my concerns about the US market as a whole. I believe that the company is on the most pragmatic path to monetizing AI. I think the B2B market will grow faster than the consumer market. But weak lending in the US currently creates more risks than opportunities.

I am withdrawing my Buy recommendation for Huntington Ingalls, Barrick Gold, Symbotic, and platinum. The reason is simple: my ideas have already worked.

I am withdrawing my Buy recommendation for Prologis because I believe that high interest rates on loans and, as a result, the weakness of all other industries except AI are still preventing my previous expectations from being realized.

Comparison of indicators

I admit that the US market as a whole has been growing. And it’s easy to get caught up in a growing market! But I am glad that the average price of my recommendations was +53% higher than the average for the US market and the S&P 500 index. However, when comparing my performance with the market as a whole, I would also compare it with the performance of the companies for which I gave Hold or Sell recommendations.

Below you can see a table showing the results for the companies I wrote articles about and recommended to Hold or Sell.

Performance Review Table (Hold & Sell Recommendations)

This portfolio of eight stocks showed an average growth rate of 18.9%, which, in my opinion, is significantly lower than the average for the stocks I recommended buying.

Summary

Trading on the market is not only about finding ideas, but also about discipline. I think that a report like this allows me to be more disciplined. Market ideas can vary, but it is important to filter them and try to find the ones that will work. I hope you found this report interesting.

Analysis of My Ideas — What Worked and What Didn’t!

My Performance Analysis Report

It’s already October, and this is the tenth month that I’ve been writing company analysis on Seeking Alpha. The fiscal year in the US ended at the end of September, and I decided to take this opportunity to report on my work. I decided to give you a report on my recommendations made in the past fiscal year. After all, it is important not only to give recommendations, but also to look back and evaluate previous analyses.

Recommendation — Buy Below you can see a table showing how the prices of stocks for which I gave Buy and Strong Buy recommendations for individual companies have changed. This selection does not include articles on macroeconomics and general market trends.

Performance Review Table (Closing price for NVIDIA is as of September 17, 2025, the publication date of the article changing the recommendation to “Hold”.)

Overall, I am satisfied with the result. The average return on 12 positions was +53.6%, based on a simple arithmetic percentage. If we convert these figures to annual returns, taking into account the holding period, the average value will be even higher.

Next, I would like to briefly go over my recommendations, describing the essence of the analysis:

AMD (+34.20%) — The idea behind the purchase is that technology giants will buy AMD chips to maintain competition in this market. Secondly, the first significant results after the chip’s announcement may only appear in early 2026, due to the time lost in customer decision-making, testing, and production queues.

As for Intel (+50.27%), I believe that the Taiwanese government’s policy of creating a silicon shield limits TSMC’s ability to compete in the US market. This gives Intel a chance to successfully implement its strategy of building new factories in the US. The company will be able to fill them with orders in the future.

As for ASML (+41.87%), the idea here is simple. This company is a critical bottleneck for the entire technology industry, as it produces lithography machines. But at the same time, it was unfairly traded at European P/E multiples rather than American ones. But I think the US will protect this company more than most of its American companies. This means that the risk factor for this company is closer to America than to Europe.

Meta’s strategy (+2.94%) simultaneously develops two directions. A long-term bet on the Metaverse and a more down-to-earth bet on open source for its AI model, Llama. But it is lagging behind in implementing this strategy. And I think that when the company manages to fully launch its AI, it can quickly take a strong position by leveraging its huge customer base.

Amazon (+3.82%) is focused on AWS and B2B customers. In my opinion, it has chosen a path with the clearest trajectory for monetizing AI in the corporate sector.

Initially, like many in the market, I viewed NVIDIA (+18.60% in 89 days) as an indispensable bottleneck for the industry for many years to come. This would imply rapid profit growth going forward. But later, I saw a threat from custom chips. Their development could shake the company’s position. Therefore, I changed my recommendation to Hold.

Alphabet (+51.77%) is probably my favorite in the AI race. Until now, the market feared that the company could lose part of its search market share due to the Microsoft/Open AI and Apple partnership. I saw that Gemini had caught up with ChatGPT in terms of quality, which, in my opinion, is a key factor in protecting its markets and actively expanding, taking advantage of its enormous size and market position.

Prologis (+18.49%): I viewed this warehouse real estate giant as a direct beneficiary of trade wars and the reshoring trend. My logic was that the complication of supply chains would lead to increased demand for modern warehouses in the US.

As for Symbotic (+192.00%), in my analysis, I wrote that this company is a leader in the implementation of AI in warehouse logistics. But its main problem is that it has only one major customer, Walmart. If the company finds new customers, it will see strong growth. And after my article was published in March, the company found a new customer. In addition to Walmart, C&S Wholesale Grocers became their second largest customer. This was the basis for the explosive growth of the company’s shares.

Last winter, I suggested buying Huntington Ingalls (+47.45%). I assumed that political tensions and the new president, Trump, would lead to increased spending on the construction of warships. And this company builds aircraft carriers. And Congress allocated money for ships, and thanks to this, Huntington Ingalls’ order portfolio grew.

A year ago, there was already a shortage of platinum (+72.10%) on the market, and this was bound to affect the price.

Problems in Africa dragged down Barrick Gold (+110.80%). But I argued that the rising price of gold would offset these problems.

Change in recommendations (Этот раздел в новом русском тексте отсутствовал, но я оставляю его нетронутым из вашего английского варианта, как вы и просили) Using this article, and so as not to write separate articles on changing my recommendations. Here I will withdraw some of my recommendations so that everything is clearly laid out in my feed. I am changing my recommendation on Amazon to Hold. The reason is my concerns about the US market as a whole. I believe that the company is on the most pragmatic path to monetizing AI. I think the B2B market will grow faster than the consumer market. But weak lending in the US currently creates more risks than opportunities. I am withdrawing my Buy recommendation for Huntington Ingalls, Barrick Gold, Symbotic, and platinum. The reason is simple: my ideas have already worked. I am withdrawing my Buy recommendation for Prologis because I believe that high interest rates on loans and, as a result, the weakness of all other industries except AI are still preventing my previous expectations from being realized.

Comparison of indicators

I admit that the US market as a whole has been growing. And it’s easy to get caught up in a growing market! Therefore, I compared the results of the companies I recommended to buy with those companies for which I gave a Hold or Sell recommendation. Below you can see a table showing the results for the companies I wrote articles about and recommended to Hold or Sell.

Performance Review Table (Hold & Sell Recommendations) This portfolio of eight stocks showed an average growth rate of 18.9%, which, in my opinion, is significantly lower than the average for the stocks I recommended buying.

Summary Trading on the market is not only about finding ideas, but also about discipline. I think that a report like this allows me to be more disciplined. Market ideas can vary, but it is important to filter them and try to find the ones that will work. I hope you found this report interesting.

Learn more about My Performance Review And A 53% Average Return