Part 1: Why did it dip? (aka Why is everyone else an idiot?)

So, your wife's boyfriend saw the chart and panicked. The stock rocketed to $185 after stellar Q1 earnings, then crashed to $63. The market thinks the party's over. Here's why they're wrong:

The "Take Rate" Misunderstanding:

• The smooth-brains saw revenue growth "slow" from 123% in Q1 to 76% in Q2 and shit their pants. They think this is a "massive deceleration." WRONG.

• That insane Q1 take rate (13.0%) was seasonal. All the Christmas shopping (Q4 GMV) gets paid off in Q1, artificially juicing the revenue number. This happens every year.

•While the paper-hands were looking at the seasonal rate, the actual business was accelerating. GMV growth sped up from 64% in Q1 to 75% in Q2. Active consumers and transactions are also up.

•Management also chose to invest in growth, like pushing the "On Demand" product (which has a lower take rate initially) to get more subscribers later. This is called playing the long game.

•The "Subprime" Ghost:

All the boomer analysts hear "subprime" and think the Big Short is happening again. This is not your daddy's 30-year NINJA loan.

•These are 6-week, small-dollar loans. The company gets its first read on a loan in 14 days, not 14 months.

•The risk isn't the whole economy; it's just new customers. The repeat customers (who make up most of the volume) are proven, loyal cash-cows.

•Sezzle can literally just turn off the new-customer tap if they see trouble. They have a big red button. Your bank doesn't.

•The Hindenburg (R.I.P. Bozo) Attack:

Remember Hindenburg? They tried to short this company into the ground in November 2024. Sezzle won, and Hindenburg literally went bankrupt. This company already had its near-death experience when it had 1-2 months of cash left and clawed its way back. Your short thesis is nothing.

Part 2: The Rocket Fuel (Why we're going to the moon 🌕)

This isn't just a comeback story; it's a "print you tendies" story.

•Papa Charlie (The Main Character): This isn't run by some diversity-hire suit. It's run by founder-CEO Charlie Youakim. He's a tech-oriented engineer who owns a massive stake and has never sold a single f*cking share. He even took a margin loan instead of selling. That's how bullish he is. 💎👐

• It. Prints. Money.

This isn't some cash-burning Silicon Valley trash. This is a profitable growth monster.

Q1 2025 Stats:

* Revenue Growth: 123% YoY

* Net Margin: 35%

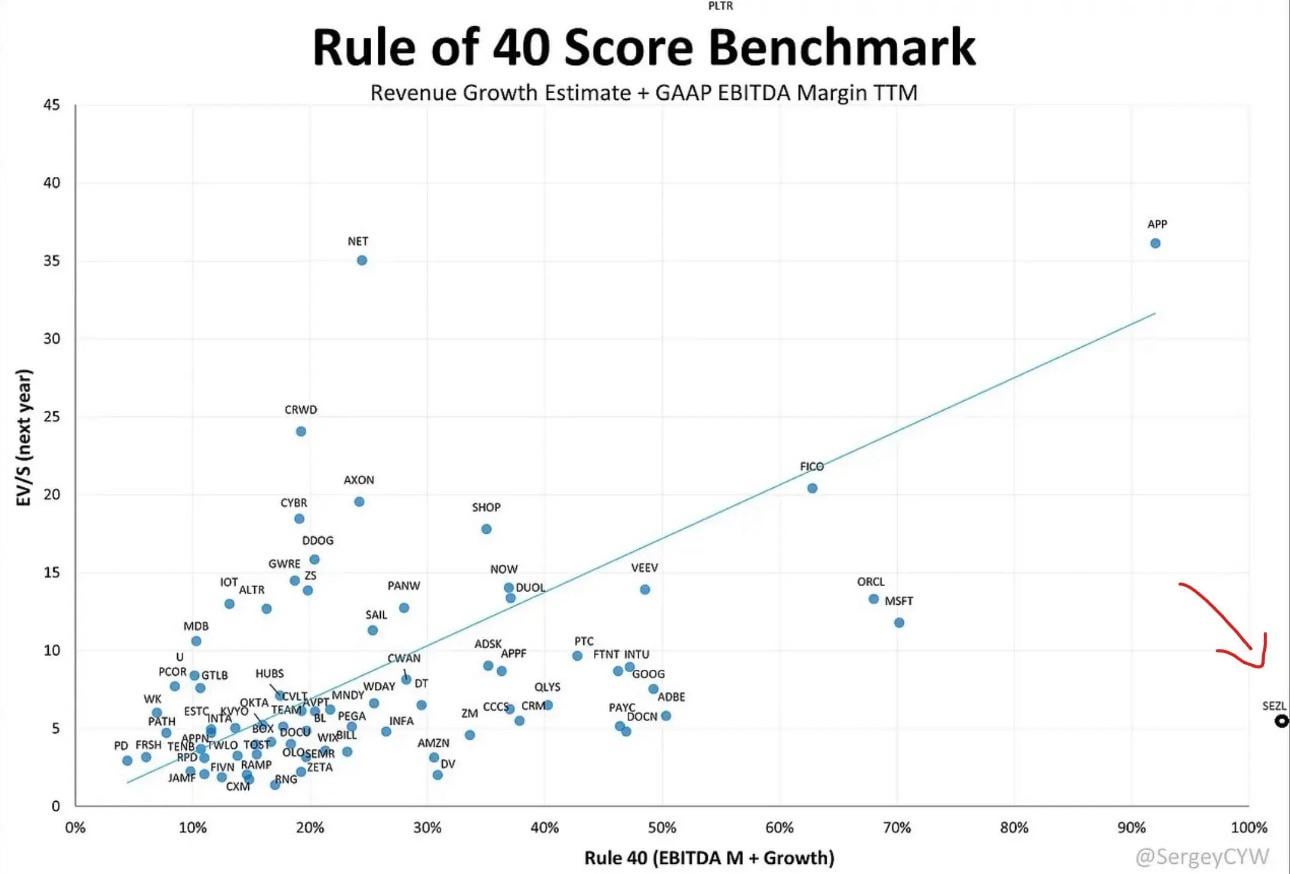

* It Broke the Goddamn Chart:

You see that "Rule of 40" image? That's the benchmark for high-quality SaaS companies. A score of 40 is good.

$SEZL's score in Q1? ONE HUNDRED AND FIFTY-EIGHT.

It's not on the chart. It's the red arrow pointing to the dot in another dimension. It's the most profitable and fastest-growing, yet the market gives it the lowest multiple.

•We Are EARLY:

Why is this golden goose so cheap? Because nobody knows it exists.

•It has only 4 analyst ratings. For a $2.5B company, that's criminally low.

•It's based in Minnesota, not some SF soy-den. The Wall Street dweebs haven't found it yet.

•The really big money is just starting to get in. Renaissance, Goldman Sachs, and Joel Greenblatt all bought in last quarter.

The market is giving you a 67% discount on the best-in-class, most profitable, founder-led company in the entire BNPL sector. The thesis paper I read is modeling a 5x to 8x MOIC (that's "Multiple on Invested Capital," for you apes) by 2027.

This isn't financial advice. I'm just an idiot on the internet. But I'm an idiot who can read.

Position

50x Jan Calls 60 strike

1000 shares @ 60.5 (bought today)